The Capital Protracted War (Draft)

Modified on 2026-01-20, first draft on 2026-01-17.

Core Idea

How to achieve class mobility through capital investment?

Use what you can afford to lose, to bet on a return you "cannot afford".

This is not about stable profits, nor is it about all-in gambling for sudden wealth. It is the optimal solution for risk-reward ratio.

There are three mainstream views in the market, but none of them can solve the problem of individual investors achieving class mobility:

- Individual Inevitable Defeat Theory - Believing one is destined to be exploited, thus avoiding the market.

- All-in Gambling for Sudden Wealth Theory - Wanting to win or lose everything in one go, leading to uncontrolled risk.

- Steady Development Theory - Wanting to get rich slowly, but lacking sufficient time.

This article proposes a fourth approach: Use the smallest acceptable risk to pursue a victory with extremely high returns.

The Problem Statement

As an individual investor, the purpose of surviving and developing in the market is to achieve sustained wealth growth, ultimately realizing the goal of class mobility.

We always yearn to discover a method for stable profits to achieve success, or fantasize about seizing an opportunity to get rich overnight. Both of these opportunities are often difficult to realize. The former because market competition is fierce and strategies can never win forever; the latter because the risk is too high and often requires a heavy bet. There are many voices, such as the "Individual Inevitable Defeat Theory" that claims one can never beat the market and investing is doomed to lose money, the "All-in Gambling for Sudden Wealth Theory" of betting everything for a chance, and the "Steady Development Theory" that wealth accumulation must rely on time. These are all erroneous views that cannot solve the problem initially posed. You can always see people getting rich overnight in the market, and also see many people going bankrupt, with some floating in the market their entire lives. Therefore, many people simplistically attribute the problem to ability or luck.

This is essentially a problem with how the issue is defined. The market has never clearly defined what the standard for "success" is. If an investor always only looks at "annualized return", "maximum drawdown", "profit-loss ratio", or "Sharpe ratio", they have never defined what the endpoint of investing is. If a return target is achieved this year, what about next year? When can the battle end? When can victory be declared? Fighting a war where victory can never be defined is destined to be impossible to succeed.

I hope to propose a new perspective on the survival and development strategy of individual investors in the market. I believe that waging a protracted war is the only way for individual investors to achieve class mobility. Briefly, a protracted war refers to a strategic combination of controllable losses, cumulative advantage, and pressing the advantage. It is not a protracted war in the temporal sense, but rather achieving leapfrog wealth growth through a publicly articulatable strategy.

- No-Risk Principle: Control the maximum speed of losses to ensure survival capability in a weak position.

- No-Waste Principle: Trade time for advantage. Use automated trading to avoid emotional decisions and achieve continuous expansion of advantage.

- No-Delay Principle: Utilize profit-based position sizing (pyramiding) to press the advantage, not wasting time, to achieve leapfrog wealth growth.

- No-Ambiguity Principle: Clearly define strategic objectives and victory conditions before committing, avoiding ambiguous strategic drift.

I firmly oppose any strategic outcome that "permanently traps individuals in the market." This is a tremendous waste of human life and social resources.

To clarify the stance, rectify the source, and distinguish it from other views, I will refute the three common erroneous views in the market one by one:

Refuting the Individual Inevitable Defeat Theory (Cynicism)

Many believe that individual investors can never beat the market and are destined to lose money.

Their reasons roughly fall into 4 points:

- Individuals' limited information is at a disadvantage compared to the market's complete information.

- Individuals' limited capital is at a disadvantage compared to the market's infinite capital.

- Individuals' limited knowledge is at a disadvantage compared to professional teams or institutions.

- There are fixed extraction mechanisms in the market, such as transaction fees, taxes, etc., which erode profit margins.

This view overlooks the learning capacity and adaptability of individual investors. The market is a game-theoretic system; exploitation and being exploited are dynamically changing and symbiotic ecological relationships. If the exploited side disappears, the exploiting side loses its basis for existence. Moreover, this ecology forms a cycle, creating a dynamic equilibrium of triangular game relationships. Often, choosing an ecological niche is key to an individual investor's success, not whether one can obtain an absolute advantage. Holders of the Individual Inevitable Defeat Theory always view the market too one-sidedly, ignoring its complexity and dynamism. This is a typical mindset of seeing a flaw and negating the entire thing.

Holders of this view often also believe that the ultimate winners are always the large institutions and professional teams. However, professional teams also started as individual investors. They grew into professional teams through continuous learning and adaptation to the market. Institutions and individuals differ only in form, scale, resources, and stage of development, not in essence. Individual investors can completely, through a protracted war, gradually accumulate experience and capital, ultimately achieving the goal of class mobility.

There is also a subtle variation among holders of this view: the belief that there might ultimately be a winner-takes-all situation, where individual investors can never survive in the market and will be completely eliminated. If this were truly the case, the exploiters would also lose their basis for existence, and the market ecology could not be sustained. Therefore, this view is also untenable.

Furthermore, this is a cynical viewpoint, attempting to evade the reality of the market by negating the capabilities of individual investors. Can individual investors truly avoid being exploited by not participating in this market? This is merely an ostrich mentality. The economy has long engulfed everyone. In today's world, most currencies are pegged to the US dollar, whose value is closely tied to US Treasury bonds, which are used to develop the United States. Many people accumulate wealth but dare not invest in the market, only to find their wealth constantly shrinking due to inflation, ultimately becoming the exploited side. In the future, even if the US falls, another country will take up its mantle and continue issuing the global reserve currency. This is unavoidable because the essence of wealth is control over resources, and wealth that cannot be exchanged for resources from others is ultimately illusory.

The world is already "chained together".

Faced with this situation, there are two choices: withdrawal from the world (出世) or engagement with the world (入世). Obviously, withdrawal is beyond the scope of this article; those who transcend need not worry about wealth. Since withdrawal is impossible, one can only engage. Individual investors must learn to survive and develop in this market. Individual investors must face the reality of the market and accept its challenges to find their place within it. Individual investors need to continuously learn and adapt to the market, gradually accumulating experience and capital, ultimately achieving the goal of class mobility.

Although individual investors are at a disadvantage in many aspects, they also have a unique political cost advantage: independence.

Any decision involving more than one interest-bearing entity faces political problems of coordination costs and conflicts of interest. Individual investors do not have these problems. The independence of individual investors allows them to adjust strategies more flexibly and focus more on their own goals without needing to consider others' interests. This independence enables individual investors to find their niche in the market and, through continuous learning and adaptation, ultimately achieve sustained wealth growth.

Obviously, in terms of investment decision-making, it's hard to say that multiple people are necessarily more advantageous than one person. From decision-making ability, financial power, execution capability, and other aspects, individual investors do not have inherent defects.

For example, here are some relative advantages stemming from the political cost advantage:

- Adaptability: Individual investors can at least choose not to participate in certain markets, or choose to learn and adapt to market changes, with no taboos. Institutions often need to maintain established business models, making rapid adjustments difficult.

- Flexibility: Allows individual investors to quickly adjust strategies to adapt to market changes without going through cumbersome approval processes. Institutions often require multi-level approvals, leading to slow responses.

- Liquidity: Individual investors can enter and exit markets almost without restriction, choosing different investment instruments and markets. Institutions are often limited by capital scale and regulatory requirements.

If individual investors can fully utilize these advantages and continuously learn and adapt to the market, they can very possibly succeed in the market. In the AI era, individual investors can use AI tools to quickly compensate for their disadvantages, such as obtaining information, analyzing data, writing code for trading strategies, etc., thereby enhancing their advantages. Especially writing code for trading strategies, as mentioned later, automated execution is key to implementing the protracted war. Even if individual investors cannot code themselves, they can use AI to assist in writing code to achieve automated trading, which is already a proven feasible solution.

Refuting the All-in Gambling for Sudden Wealth Theory (Opportunism)

On the other hand, a minority in the market advocate a "bet it all for a chance" strategy, believing that a one-time high-risk investment can achieve rapid wealth growth. This strategy seems to solve the time problem of personal wealth growth but actually ignores the importance of risk management. Those who hold this view and act on it are either novices uninitiated by the market or desperate gamblers with little left to lose. They often believe their luck can overcome market risks, but reality is often otherwise.

All-in investments often come with enormous risks. Once they fail, they can lead to severe personal wealth loss or even bankruptcy. Moreover, opportunities in the market are not something everyone can grasp; the probability of success is often very low. Therefore, relying solely on an all-in investment strategy cannot guarantee sustained personal wealth growth and may instead lead to rapid wealth depletion. Currently, in the MEME market, there are many myths of sudden wealth, with stories of overnight thousand-fold or ten-thousand-fold gains emerging endlessly, attracting a large number of speculators into the market. However, these stories often ignore the underlying risks and failure cases, leading many speculators chasing the dream of sudden wealth to ultimately end up bankrupt.

Some people appear to go all-in, but the actual funds they invest each time are not their entire capital, but all the funds they have on the table. Even if they lose, they have reserves. These are not the holders of the All-in Gambling for Sudden Wealth Theory we wish to discuss. However, under certain conditions, such people can also become true all-in investors, for example, when the funds on their table are close to their total capital. Those accustomed to all-in investing are increasingly likely to become true all-in investors.

Comparatively, most people understand this principle. But when opportunities arise, they are often too quickly overwhelmed by the desire for sudden wealth, transforming into all-in investors. This is the most common mistake individual investors make during the future strategic stalemate phase. It is necessary to prepare psychologically in advance to prevent losing rationality and making wrong decisions when opportunities come.

This is both a crisis and an opportunity. The more people advocate all-in gambling for sudden wealth, the more it indicates the existence of huge volatility and immense opportunities in the market. The more enthusiastic people are about gambling, the more they can perceive the existence of high-volatility markets. Individual investors need to clearly recognize that all-in investment strategies cannot guarantee sustained personal wealth growth and may instead lead to rapid wealth depletion. However, if one can moderately utilize all-in strategies under the premise of controllable risk, then individual investors can very possibly achieve rapid wealth growth in the market.

Refuting the Steady Development Theory (Dogmatism)

The last, and most classic, viewpoint. I criticize it as representative of dogmatism. It presents seemingly reasonable arguments to prove that personal wealth growth must rely on steady development strategies. However, this view ignores the time constraint problem of personal wealth growth. There are also many popular sayings, such as "be a friend of time," "the magic of compound interest," etc., which all sound very reasonable.

Historically, dismantling dogmatism has always been difficult because it often wears the cloak of rationality, making it hard to discern its true nature.

The living legend—Warren Buffett, the pioneer of value investing—is the greatest representative of this view. He advocates achieving steady annual growth of around 20% by holding quality assets long-term. This view is indeed applicable to a certain extent for institutional investors and most individual investors. However, it does not solve the fundamental contradiction in the problem of individual wealth class mobility—the conflict between the finite nature of an individual's lifespan and the time required to accumulate wealth.

In this world, there are many people as long-lived as Buffett, but only one "Oracle of Omaha." There are also many people who know and practice value investing. If everyone could develop smoothly as if "serving time," where would the extra money come from? If you can accumulate wealth over time, then your predecessors, who came before you, can do so even more. Every individual investor should seriously consider whether they have overlooked some blind spot. In this world, are there invisible barriers hindering wealth growth? If so, what are they? If not, why can't most people achieve leapfrog wealth growth?

The fundamental dilemma faced by individual investors is:

- Wanting steady growth, but steadily growing wealth cannot keep up with annually increasing living expenses. One cannot accumulate wealth without eating or drinking.

- Wanting to increase accumulation, but accumulation plans are always interrupted by sudden risk events—unemployment, illness, or family变故.

- Wanting to lie low and develop, but social pressures催促 improving quality of life—buying a house, a car, getting married, having children, maintaining appearances, etc.

- Wanting to take a chance, but fearing the loss of existing accumulation, unable to bear the risks of large fluctuations.

There are many theories in the market teaching how to make wealth grow steadily, how to avoid risks, how to earn 10-30% returns every year. Such strategies include but are not limited to:

- Value Investing: Selecting undervalued quality assets, holding them long-term, waiting for the market to correct their price.

- Risk Parity & Permanent Portfolio: Diversifying investments across different asset classes,定期 rebalancing, reducing overall portfolio risk.

- Index Investing: Investing in market indices to obtain the market's average return, avoiding individual stock risk, growing in sync with the national economy's macro environment.

If so, by the time assets increase tenfold, it will be ten years later, life will have entered the next stage, and as life stabilizes, the significance of wealth growth diminishes. If an individual relies solely on steady development strategies to achieve wealth growth, it is likely that leapfrog wealth growth cannot be achieved before the end of their lifespan. And if wealth does not arrive when the individual needs it most, when one is old, is pursuing leapfrog wealth growth still meaningful? Isn't having enough sufficient?

Some may fantasize about achieving wealth growth for future generations through inheritance, using that as their own purpose. However, "children selling their ancestors' land without heartache"—this thinking is very unrealistic. Each generation has its own奋斗 goals and lifestyle. Future generations may not cherish the wealth accumulated by predecessors and may even squander it. Therefore, leaving wealth to the next generation is not necessarily meaningful. Inheritance is meaningful only when both wealth and ideas are passed down. In fact, the transmission of ideas is more important, the main thing.

The scenario for steady development is completely different from that of ordinary people. I emphasize that I am refuting those dogmatic views that advocate steady development under any circumstances. Refuting the Steady Development Theory may sound heretical, but in reality, for individual investors, steady development is not a pragmatic choice. Individual investors need to clearly recognize that the time for wealth growth is limited, and steady development strategies often cannot achieve leapfrog wealth growth within that limited time. Therefore, individual investors need to find a strategy that can achieve wealth growth in a relatively short period, not just rely on steady development strategies.

Of course, contradictions transform—when personal wealth reaches a certain scale, steady development strategies become more important because the wealth is already sufficient to support personal living needs. Steady development strategies can help individuals maintain stable wealth growth, avoiding wealth loss due to market fluctuations. Moreover, as a base for the next round of wealth growth, steady development strategies can provide individuals with a base area, preparing for another battle for class mobility.

However, before personal wealth reaches a certain scale, steady development strategies are not the best choice for individual investors to achieve wealth growth. Individual investors need to find a strategy that can achieve wealth growth in a relatively short period, not just rely on steady development strategies.

The Capital Protracted War

The protracted war I speak of does not mean a war of attrition in the temporal sense, but achieving leapfrog wealth growth through a publicly articulatable strategy. It consists of several aspects:

- Learn to correctly analyze the contradictions between the enemy and ourselves and the situation, thereby formulating correct strategic guidelines.

- Prepare a stable cash flow input, control the maximum speed of losses, thereby achieving survival in a weak position.

- Learn to maintain cumulative advantage, avoid unnecessary time消耗 from watching the market, thereby achieving continuous expansion of advantage.

- Learn to press the advantage and fight decisive battles at the right moment, not missing historical opportunity windows.

- Establish psychological expectations, accept the possibility of ending up with nothing gained, thereby avoiding psychological breakdown due to failure.

Mathematical Interpretation

This theory has a mathematical interpretation:

First, set the victory condition as wealth reaching a certain value . The goal of all strategy is to achieve this victory condition. This victory condition differs for each person, depending on individual living needs and wealth goals.

Second, assume there exists a strategy , which is a black-box investment machine. It inputs capital at time and outputs capital at time . We can define this strategy function with 3 parameters. Once these 3 parameters are determined, the output capital is determined:

This function is not a mathematical function with an analytical expression, but an abstract representation of a black-box investment machine. Its inputs are a time period and capital; its output is capital. Moreover, in also has an objective domain , i.e., . This represents the lower and upper limits of investment capital. Individual investors cannot invest less than or more than . represents the market's minimum transaction amount; represents the market's capital capacity for this strategy.

Clearly, this defines a basic investment concept: between time and , investing capital yields capital . If , the strategy is profitable; if , it is loss-making.

Now, define our capital curve , representing the total profit/loss at time . Our goal is for the capital curve to reach the victory condition at some time .

Now, at our initial investment time , we first need to define a bottom-line risk control line:

Here, is a constant representing the maximum loss speed we can承受. The meaning of this risk control line is that we must ensure that at any time , our capital curve does not fall below this line. This ensures our survival capability in a weak position. The setting of varies from person to person, depending on individual cash flow capability. For example, investing 3000 yuan per month means yuan/day.

An investment action can be defined as using strategy to invest capital () during a time period , thereby obtaining capital . This action can be expressed as:

Our goal is to, through a series of investment actions, ultimately make the capital curve reach the victory condition at some time , while ensuring that at any time , the capital curve does not fall below the risk control line.

Furthermore, we can define profit as the floating profit above the risk control line:

You will find that even without any investment action, grows linearly over time. This is because the risk control line itself declines linearly, while the capital curve remains unchanged without investment actions. Therefore, grows linearly over time.

When reaches , we can use all of as the investment capital for the next investment action. This is the so-called profit-based position sizing (pyramiding) strategy.

This strategy, under continuous profitable conditions, can achieve rapid growth of the capital curve , thereby achieving leapfrog wealth growth. Because our purpose is to make , the only other outcome is , which means the capital curve directly declines along the risk control line, waiting for the next opportunity.

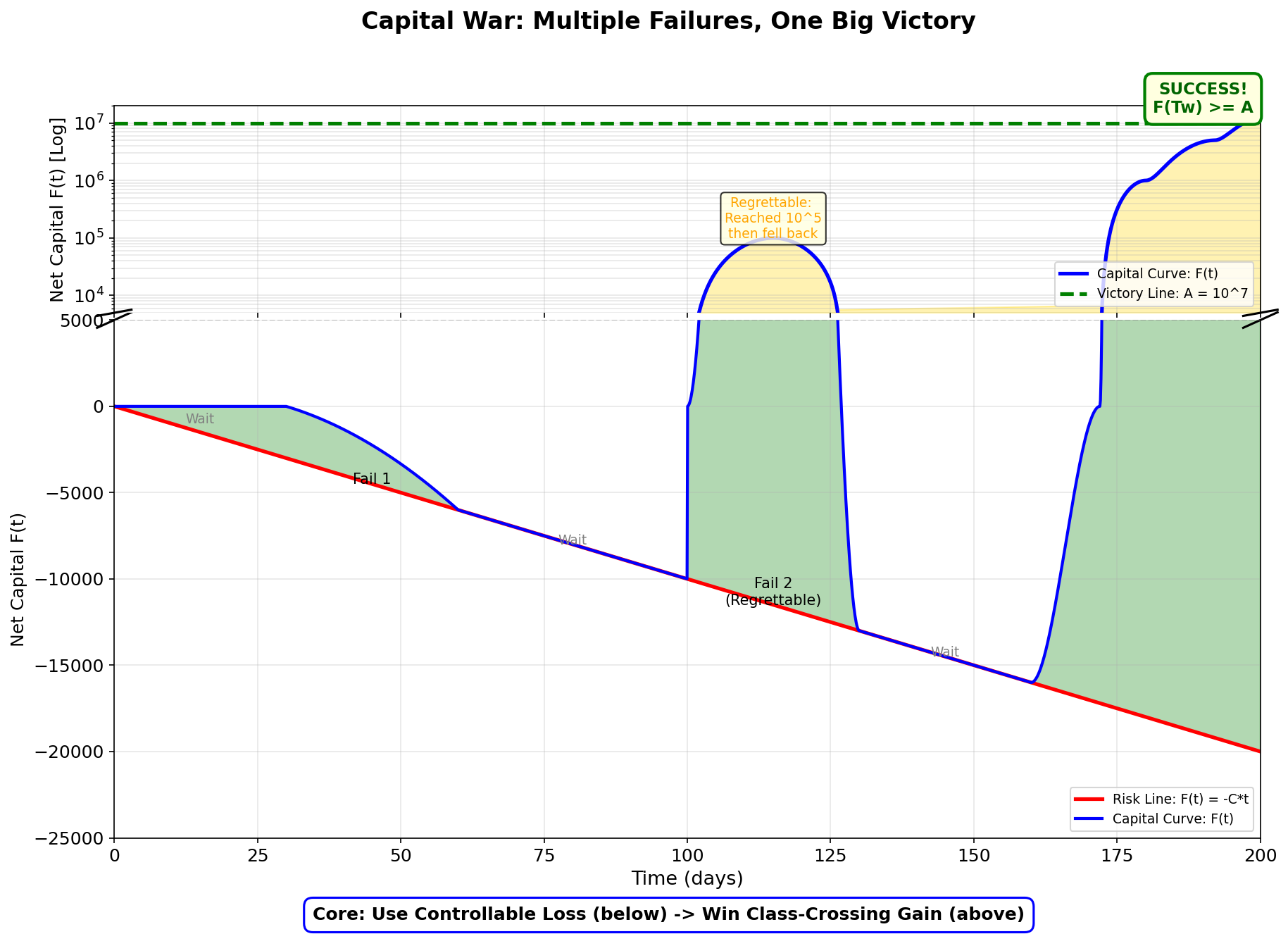

This diagram illustrates the typical path for an individual investor to achieve successful class mobility in the market.

The horizontal axis is time (days), and the vertical axis is net capital F(t).

The diagram contains two key lines:

- 🔴 Red Risk Control Line : Represents the maximum loss boundary you can承受.

- 🟢 Green Victory Line : Represents the goal of class mobility.

- 🔵 The capital curve (blue) goes through three phases:

- Fail 1: Starting from the origin, the first attempt fails, losses touch the risk control line and stop.

- Fail 2 (Regrettable Failure): The second attempt briefly突破 to , but ultimately falls back to the risk control line due to market reversal. This is the most残酷 situation—you were once close to success but failed due to not adhering to the strategy.

- Success: After sufficient waiting and preparation, finally启动 from the risk control line, successfully突破 the victory line .

Core Insight: Success is not about being right every time, but using controllable small losses to换取 one big victory for class mobility. Most time is spent waiting and testing; decisive action is taken at critical moments.

Next, for the victory target , strategy , and risk control line parameter , we can construct a全新的 backtesting evaluation system.

Measure how long strategy takes to achieve victory target , denoted as . This time is a random variable, depending on the performance of strategy and market volatility. To simplify, assume A = 10 million, C = 100 yuan/day. Evaluation shows that in 5 years of history, strategy S on average achieves victory target A once per year. This means you need to invest 100 yuan/day for 1 year, possibly catching one opportunity to earn 10 million. Your cost is 36500 yuan/year, and the收益 is 10 million. Clearly, this is a very划算 investment; you would be very patient when investing. But what if it happens only once every 5 years? Once every 10 years? Then it's not划算, the risk is high. Folks, I just have one sentence: how many decades does a person have?

Now, based on one's own resources, evaluate the expectation of achieving victory under different conditions, then invest. If deemed unacceptable, do not invest. Then spend time optimizing strategy S, improving its win rate, reducing the time needed to achieve victory target A. This process is one of continuous optimization and adjustment until a strategy S is found that can achieve victory target A within an acceptable time frame.

This is the mathematical interpretation of the Capital Protracted War.

Practical Rules

It sounds complex, but in practice, it's simple.

- Must prepare a cash flow input. Use time cost to换取 information and experience advantage. There must be a continuous, controllable cash flow that can be invested. This can be salary income or stable interest income. This cash flow doesn't need to be large, but must be stable. With this cash flow, one can continuously make small investments in the market, accumulating information and experience advantage.

- Must use automated trading methods for underlying investment operations, avoiding any emotional or humanly unsustainable decisions, preventing discipline issues at the execution stage. Moreover, automated trading saves individual investors' energy, reducing psychological pressure from regretting exiting to保本. Do not pursue a fully automatic system, but pursue an imperfectly profitable yet省心的 system. Investors must focus their energy on designing and optimizing programmatic strategies. If you can't code, let AI help. Don't watch the market, don't纠结 over whether to buy or sell in each trade. This doesn't liberate you; it tortures you. This is the key to what I call advantage accumulation and avoiding unnecessary消耗.

- Profits must be immediately used for position sizing. When capital is invested in the correct direction, profits will quickly appear. Utilize the profit-based position sizing (pyramiding) strategy to continuously扩大 advantage. Note: there is a very strict stop-loss condition here: if losses reach the level before sizing up, must stop loss. This is because market volatility clusters; tailwinds and headwinds often cluster. If one can抓住 tailwind clustering opportunities, then the profit-based position sizing strategy can be used to continuously扩大 advantage. Sizing up means your cost basis rises, and the buffer between the cost basis and the current net value line constitutes a safety buffer. When the buffer shrinks, if the current speed is still too fast, the program should trigger position reduction to prevent being wiped out.

This endeavor ultimately has two outcomes: one, successfully achieving leapfrog wealth growth; two, failing with limited losses. Regardless of the outcome, individual investors can accept it坦然, learn, and grow from it.

Responding to Some Common Questions

Does the Capital Protracted War negate the power of compound interest?

No,恰恰相反. The Capital Protracted War maximizes the power of compound interest. Buffett's compound interest is extremely conservative compared to the Capital Protracted War. The Capital Protracted War uses controllable losses to bet on an extremely high return, achieving leapfrog wealth growth. In this way, the power of compound interest is maximized.

Only末日轮 options, lottery tickets, and prediction markets (like PolyMarket) can achieve similar effects, but market choices are currently still too limited, and pricing is not cheap.

What's the difference between the Capital Protracted War and regularly buying lottery tickets?

The difference from regularly buying lottery tickets is that lottery is a purely random event with no controllability. The Capital Protracted War can improve the win rate by refining the strategy, thereby increasing the probability of achieving the victory target. Lottery odds are often fixed, while the Capital Protracted War can continuously adjust and optimize the strategy to improve the win rate.

What if everyone adopted the Capital Protracted War strategy?

The competitive pressure among implementers of the Capital Protracted War cannot be very high. Because only those with the same market direction judgment at the same moment would form direct competition.

- Strategic purposes differ. Those not aiming for class mobility will not adopt the Capital Protracted War strategy. A considerable number of people will adopt steady growth strategies to maintain stable wealth growth. Their existence also reduces competitive pressure for the Capital Protracted War strategy. Their existence can actually serve as counterparties, creating victory opportunities for us.

- Diversity of strategy S. Strategy S is private; different people are unlikely to adopt exactly the same strategy S. Even similar strategies S will produce different results due to different parameters. This diversity means implementers of the Capital Protracted War strategy will not form direct competitive relationships. However, some crowding effect still exists.

- Differences in victory target A and risk control parameter C. These two parameters determine the启动 rate of position sizing. This leads to differences in the actual investment intensity of different investors at the same point in time, differentiating their performance.

Market opportunities change dynamically; different strategies S will obtain different opportunities at different times. The market will scatter these opportunities, forming a dynamic ecosystem.

How to determine the cash flow C?

First, one needs to correctly understand margin and leverage.

A practical question: if one拿出 6000 yuan per month, approximately 200 yuan/day investment额度, what can one buy? Almost nothing.

This misunderstands the concept of cash flow; it's for covering losses. For example, buying one lot requires 10,000 yuan. Your 200 yuan cash flow means you can accept a 2% loss speed per day, which is actually not little. If it exceeds this speed, you need to actively exit the market to prevent excessive losses.

This differs from another investment style: saving tens of thousands over several months, investing it all at once, not setting stop-loss,不敢认输 when losing, watching one's底线被市场摁在地上摩擦; when profiting, desperately adding positions,生怕 missing发财的机会, ending up stuck at the山顶, becoming山顶 capital. This is completely失控, lamentable.

Determining position size based on potential loss is a basic capital management concept. For this,学好 elementary math and correctly solving word problems is necessary.

Difference from "Heavy Betting When Seeing an Opportunity"

The Capital Protracted War strategy does not rely on subjective "seeing an opportunity," but on the objective "profit-based position sizing."

It does not rely on an artistic subjective judgment but on a mechanical objective rule. The executor only needs to follow the rule, waiting for opportunities to arrive, without needing to judge whether opportunities exist. The executor must be a programmatic system, avoiding human emotional interference.

Furthermore, in the Capital Protracted War strategy, heavy betting is actually not allowed without floating profits. Heavy betting is only allowed when there are floating profits. This is because floating profits represent the market's认可 of strategy S. Heavy betting without floating profits often leads to unbearable losses.

Below the risk control line falls into the realm of机会主义 with失控 risk. This is what the Capital Protracted War aims to avoid.

Relationship between the Capital Protracted War and Steady Growth?

They are mutually transformable. The key is that investors must clearly define their strategic objectives.

When individual investors achieve leapfrog wealth growth, they can choose to转移部分资金 to steady growth strategies to maintain stable wealth growth. Steady growth strategies can help individual investors avoid wealth loss due to market fluctuations, achieving long-term stable wealth growth. Steady growth strategies can serve as a base for the next round of wealth growth, providing individual investors with a base area, preparing for another battle for class mobility.

Summary

The key points summarized are:

The framework remains unchanged; strategies can be swapped. The core is using controllable losses to换取 uncertain large收益.

- Start with cash flow, control loss speed, achieve survival in a weak position.

- Use automated trading, avoid emotional decisions, achieve continuous expansion of advantage.

- Utilize profit-based position sizing, press the advantage, achieve leapfrog wealth growth. Even if it fails, the loss equals the loss before sizing up,不会击穿 cash flow.

The specific programmatic strategy is the decisive key. The core of this article lies in redefining the goal and criteria for victory, thereby providing individual investors with a feasible strategic path to achieve leapfrog wealth growth.

Please look forward to my subsequent articles, which will propose a specific testing framework to verify the feasibility of this theory. Let's see whether back then I added too little position, or the strategy wasn't good enough. One of these two must be the conclusion.